Index provider Stoxx announced an interesting new benchmark – the Stoxx Global 1800 EM Exposed Index. In brief, this is a sub-index of its Stoxx 1800 Global Index (which holds 1,800 developed world stocks) focusing on companies that get a substantial portion (at least 33%) of their revenues from emerging markets.

The press release [PDF] has a bit more detail, as does the index data page on the Stoxx site (although there isn’t much data up yet). Conceptually, this is pretty similar to the Russell Geographic Exposure Index series launched in September.

In both cases, the idea is that you can get exposure to EM growth through developed world stocks that offer better liquidity, corporate governance and other desirable factors. It’s a fairly popular theme and with two related indices launched in the last few months there’s a good chance that we will see an exchange-traded fund based on it sooner or later.

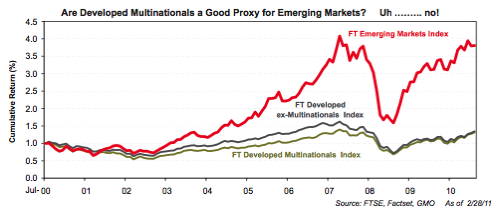

That said, while there is some logic to the underlying idea, I have reservations about embracing this kind of approach too wholeheartedly. For a start, in contrast to what many investors think, getting EM exposure through multinational large caps has not delivered the same returns as buying EMs directly, as the chart below from Arjun Divecha at GMO shows oclearly.

(This chart comes from a short note called The Gratuitous Use of Statistics, which is on the GMO website. Registration is required but is free and worth doing – the GMO team produce some very thoughtful material.)

In addition, picking companies that have high revenue exposure to EMs is not the same thing as getting high-quality unique growth from EMs. Obviously, revenue does not equal profit and you can have high revenue exposure and yet be losing money on EM ventures.

More subtly, geographically screening can be misleading on what kind of otherwise-unobtainable exposure you get. For example, it may select a business such as an oil company that has a high geographical revenue share from EMs. However, the price of oil is (mostly) a global price – so this company would not give you any EM exposure that is not already incorporated in the oil price received by any another company elsewhere in the world (ie EMs may affect the price of oil, but you don’t need an oil stock that does business in EMs to get that price impact).

In fact, you might get better EM exposure from multinationals by simply looking at global indices for sectors such consumer staples or healthcare. These indices typically include many companies with significant exposure to EMs and they are arguably the businesses that have been most successful in getting value out of their EM operations over time.