“Quality” is clearly a popular theme among nervous equity investors at the moment, so it’s not surprising to see that MSCI has just launched a series of quality indices. The press release [PDF] and methodology [PDF] give more details, but essentially the components are screened on three factors: High return on equity, stable earnings and low financial leverage.

This is what most investors would consider to be a simple standard definition of quality, as opposed to the two obvious comparison indices: Société Générale’s new-ish Global Quality Income Index (which is a somewhat more complicated combination of the Piotroski score and the Merton distance-to-default model) and the older Standard and Poor’s S&P 500 High Quality Rankings Index, which is based on stability and growth of earnings and dividends (and in my view doesn’t seems to provide a very satisfactory quality filter).

The MSCI series includes five indices:

- MSCI World Quality – start date November 30, 1981

- MSCI ACWI Quality [ACWI means All Country World Index or World including emerging markets – the standard World index includes developed markets only] – start date November 30, 1998

- MSCI Emerging Markets Quality – start date November 30, 1998

- MSCI Europe Quality – start date November 30, 1981

- MSCI USA Quality – start date November 30, 1981

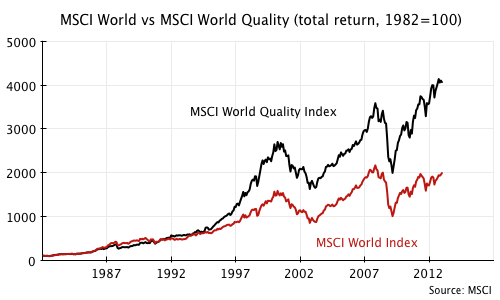

As usual, historical performance data can be found on the MSCI website. I haven’t looked at it in detail yet, but one obvious point stands out. In every case, the high quality index has delivered better long-term price return and total return than the standard market index.

As the MSCI World and MSCI World Quality chart below shows, the extent of outperformance can be substantial over time. The difference for the EM and ACWI series, with their shorter history, is smaller and mostly arises from the last few years, but it still seems to be evident.

This is not unexpected. As discussed in previous articles, there is quite a bit of evidence to suggest that higher risk correlates with higher returns across asset classes, but does not reliably do so within asset classes. Safer, high quality companies seem to outperform their riskier peers, in breach of standard finance theory, for reasons that may be rooted in investor psychology and the preference for exciting “lottery ticket” stocks.

The arrival of dedicated quality indices from one of the major index providers implies we’re likely to see ETFs or other index-tracking products based on it at some point. Providers such as BlackRock have already embraced minimum volatility indices and quality is probably an easier sell, to the retail market at least.

Obviously, there’s no guarantee that these indices will outperform the wider market from this point on – arguably, quality stocks are more expensive relative to their peers than usual. But given that most investors probably buy quality for safety rather than because they expect outperformance, that’s not necessarily a problem for continued interest in quality strategies.